₹499

₹599

17% off

You save ₹100

Inclusive of all taxes

16 people viewing now

Shop with peace of mind

Make it special+₹ 49.00

Gift Wrapping (Prepaid Orders Only)

Add a clean, gift-ready wrap with your order.

Qty

Added to cart successfully.

Bulk / wholesale enquiry

Tell us how many you need and we'll send you our best price on WhatsApp.

Opens WhatsApp with your details pre-filled. We reply with the best price.

Offers

Frequently bought together

Total:

Product Highlights

Full specifications at a glance

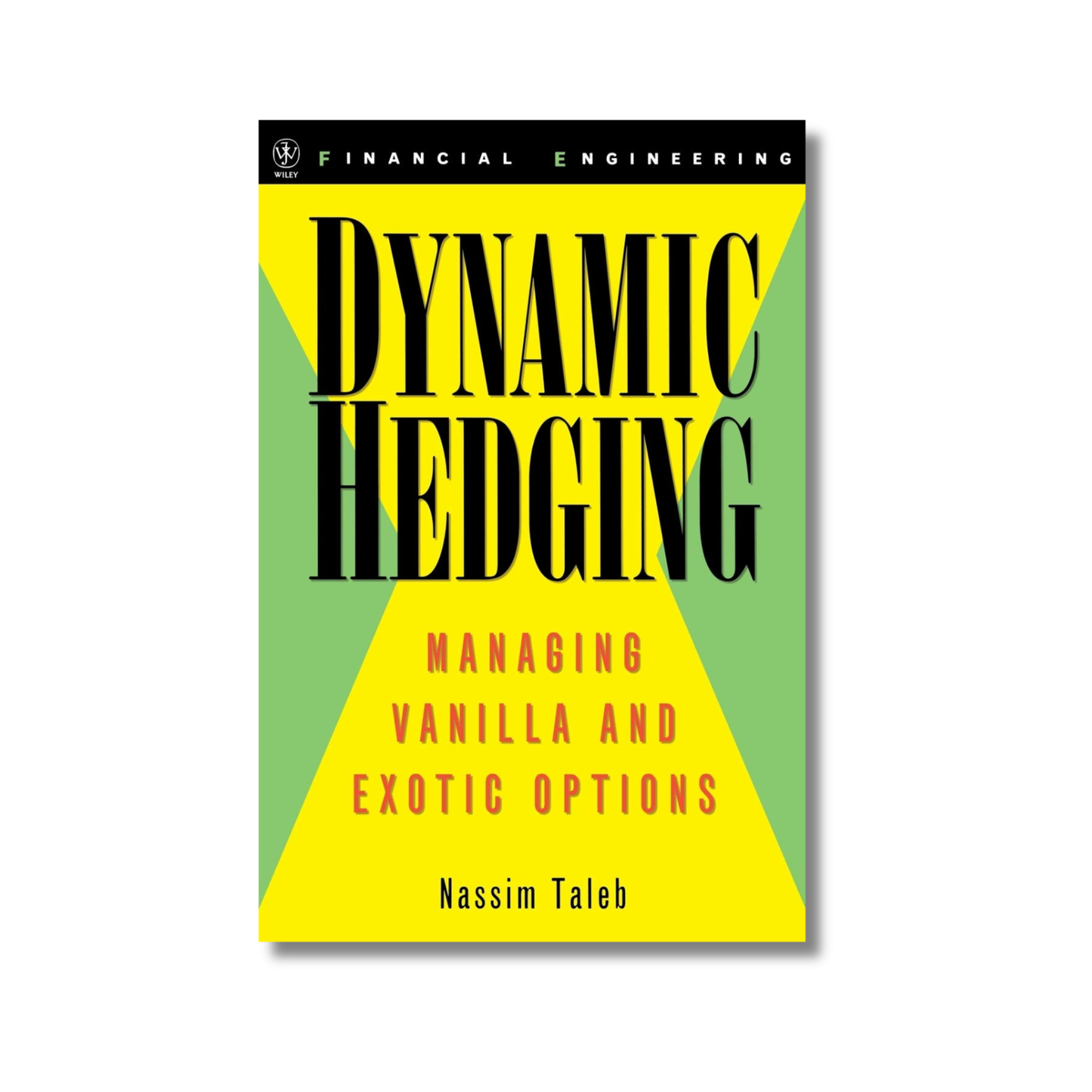

Publisher

Wiley

Language

English

Hardcover

528 pages (May Vary)

ISBN-10

0471152803

ISBN-13

978-0471152804

Nassim Nicholas Taleb spent more than two decades as a risk taker before becoming a full-time essayist and scholar focusing on practical, philosophical, and mathematical problems with chance, luck, and probability. His focus in on how different systems handle disorder. He now spends most of his time in the intense seclusion of his study, or...

More by this author · 3 in store